The New DTC Playbook Has a Storefront

Why CPG Brands Want Restaurants and Retail Now and Investors haven't caught up.

For the last decade, the cleanest consumer-brand story was direct-to-consumer.

Cut out the middleman. Own the customer. Build online. Avoid the shelf, brokers, distributors, slotting fees, chargebacks, and the slow politics of grocery retail. If the product was good enough and the brand was sharp enough, the internet would do the rest.

That story was not wrong. It was incomplete.

What many brands eventually learned is that owning a website is not the same thing as owning trust. A customer can see your ad, like your packaging, read your founder story, get retargeted for three weeks, and still not buy. Or they buy once, decide the product is fine, and disappear into the fog of modern attribution.

Food has an even harder version of this problem. You can sell eyewear online with a home try-on program. You can sell software with a demo. You can sell mattresses with a return policy. But food requires a different kind of belief. The customer is buying taste, freshness, safety, quality, portion size, preparation, and often a premium they need to justify before checkout.

That is why restaurants and retail are back in the conversation.

Not because every CPG brand should become a restaurant company. Most should not. Restaurants remain brutally difficult businesses: labor, rent, food cost, insurance, repairs, training, turnover, waste, permitting, and thin margins. Retail is not easy either. Stores come with leases, buildouts, inventory risk, staffing, shrink, local execution, and the daily discipline of operating in the physical world.

But physical experience solves a problem that ads, websites, and grocery shelves do not solve very well. It helps a customer believe.

The grocery shelf still matters. Distribution can create enormous scale. But the shelf is a bad classroom. It gives a brand a few inches of space, a price tag, maybe a discount, and a few seconds of attention from a customer who probably entered the store with a list, a habit, and a default brand already in mind. For a premium, unfamiliar, or story-driven product, that is a weak environment for persuasion.

It is also an expensive one. NIQ says initial slotting fees are generally around $250 to $1,000 per item per store, and that number can climb quickly across regional launches or high-demand markets. Private label has also become a much more serious competitor. Circana reported that U.S. private-label CPG sales reached $330 billion, with private label taking a 24% unit share and 23% dollar share. Store brands are no longer just cheap alternatives; in many categories, they are credible products backed by the retailer’s own trust.

So yes, getting on the shelf still matters. But presence is not persuasion. Distribution is not demand. A brand can win the right to sit on the shelf and still lose the customer.

Restaurants, cafés, boutiques, and showrooms do something different. They create context. A product on a shelf is an object. A product inside a physical experience becomes part of a world.

This is the Warby Parker lesson. Warby Parker did not abandon e-commerce when it opened stores. It made e-commerce less risky. In its S-1, the company said its retail stores “embody our brand, drive brand awareness, and serve as efficient customer acquisition vehicles.” The store was not just a place to transact. It was a place to reduce friction.

Customers could touch the product, understand the fit, interact with the brand, get an eye exam, and build confidence. The physical footprint did not contradict the digital strategy. It made the digital strategy more believable.

Food brands should study that carefully. The question is not online or offline. That is an outdated debate. The better question is: where does the customer become comfortable enough to buy, repeat, and recommend?

At Meat N’ Bone, we learned this in a very practical way. Premium proteins are not easy to sell purely online. A customer can look at photos of Japanese A5, USDA Prime, Australian Wagyu, Iberico pork, lamb, seafood, or game meats, but photos only go so far. They want to see marbling. They want to ask questions. They want to understand grades, cuts, cooking methods, portions, and whether the product is actually worth the premium.

A website can explain some of that. A boutique explains it faster.

The boutiques became more than stores. They became trust infrastructure. A customer could walk in, see the product, talk to the team, ask what to buy for dinner, understand why one cut costs more than another, and leave with confidence. That confidence traveled back into e-commerce, catering, gifting, local delivery, subscriptions, and repeat purchasing. Once the customer believed the brand physically, ordering online became less of a leap.

The restaurant side did something similar, but with a different job. A boutique can show the product. A restaurant can prove it. A steak on a website is inventory. A steak cooked properly, served correctly, and experienced at the table is evidence. It tells the customer, without a long explanation, that the product is real, the quality is there, and the brand knows what it is doing.

This has also been one of the more interesting parts of our fundraising journey.

When we talk to investors, a common question is some version of: why do you have boutiques? Why do you have restaurants? Why not stay cleaner, lighter, more purely e-commerce?

It is a fair question. Physical locations add complexity. Restaurants add even more. From a distance, the model can look less elegant than a pure DTC business with a website, a warehouse, and a paid-media engine.

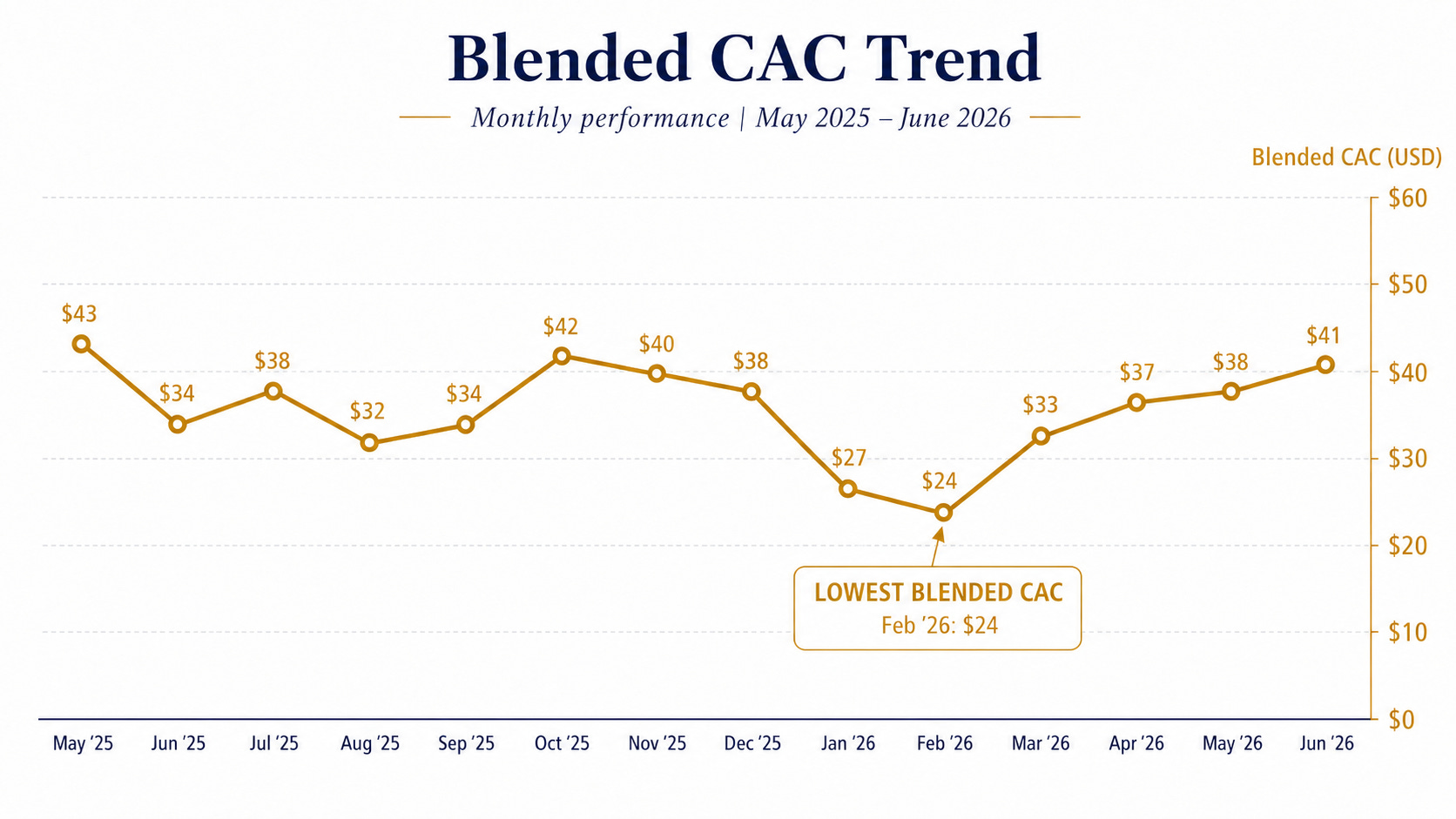

But the question they often do not ask is the more important one: why is your customer acquisition cost so much lower than many of your competitors?

That is where the answer gets interesting.

The boutiques and restaurants are part of the reason. They are not just cost centers or side businesses. They are part of the acquisition system. They create local awareness. They let people experience the product. They create confidence. They generate content. They turn customers into repeat customers. They make the online business easier to trust.

What is funny is that when we explain this to marketing people, especially digital marketing people, they usually understand it immediately. Their reaction is often: wait, that is actually genius.

Because they live every day with the broken math of digital acquisition. They know how expensive paid social has become. They know attribution is imperfect. They know a click is not trust. So when they see a physical store or restaurant that can create demand, lower friction, and improve repeat behavior across channels, they understand that it is not just “retail.” It is media. It is sampling. It is conversion. It is retention.

The disconnect is that operators and marketers often see the system, while some investors still see the pieces. They see a boutique, a restaurant, and an e-commerce business as separate units. But to the customer, it is one brand. They may discover us through social, walk into a boutique, eat at the restaurant, send a gift online, reorder through email, and then recommend us to a friend. That is not messy. That is how people actually buy.

This is where the CAC conversation gets interesting.

On paper, retail looks expensive. Rent, payroll, utilities, insurance, buildout, inventory, and local management all hit the P&L before the first customer walks in. A Meta ad looks cleaner. You spend money, track a click, and pretend attribution is precise.

But that comparison can be misleading. A good store is not only a place where transactions happen. It is a local billboard, a showroom, a sampling station, a service desk, a content set, a trust engine, and a repeat-purchase reminder. The rent is not just rent. Part of it is marketing. Part of it is customer service. Part of it is education. Part of it is retention.

For a brand with 400 SKUs and high rotation like Meat N’ Bone, it just makes sense.

This does not mean every store lowers CAC. Bad retail burns capital. Bad locations, weak teams, poor merchandising, and unclear strategy can turn physical expansion into a vanity trap. But good retail can lower blended CAC because it turns fixed rent into recurring acquisition. Every walk-in, conversation, tasting, local search, photo, and repeat visit compounds.

Food can be even stronger than eyewear here because the product is sensory. A customer who tastes something, asks questions, sees the quality, or has a great meal is not the same as a customer who clicked an ad. The physical interaction carries more trust. It reduces uncertainty. It makes the first purchase easier and the second purchase more likely.

Oatly understood this well. Its foodservice-led strategy used specialty coffee as a trusted environment to build awareness and drive retail demand. In its F-1, the company wrote that consumers discover Oatly in “an expertly brewed cup of coffee or cappuccino from their favorite coffee shop,” and that the experience can lead to grocery purchase.

That is not random sampling. That is channel design.

The same logic shows up across the market in different forms. A café can make a coffee brand feel real. A restaurant can showcase an alternative-protein portfolio. A branded counter can test flavors and packaging. A boutique can make a premium product less intimidating. A shop-in-shop can borrow traffic and credibility from a larger retailer. These are not identical strategies, but they share the same logic: the product becomes stronger when the consumer experiences it in context.

The mistake is confusing context with cool. A restaurant that exists only because it looks good on Instagram is usually an expensive mistake. A store that does not clarify the customer journey is just another rent bill. Physical retail has to be assigned a job.

Is it a showroom? A sampling engine? A product lab? A content studio? A flagship? A customer-service hub? A wholesale lead generator? A way to make e-commerce feel safer?

Those are different strategies, and they should be measured differently. A butcher shop may be valuable not only because of four-wall revenue, but because it creates confidence in the online cold-chain promise. A restaurant may be worth doing if it proves the product, creates content, trains the customer, and makes the brand more credible across every other channel.

But if the physical layer does not make the rest of the business stronger, it is probably vanity. The restaurant industry is too hard for vibes. Retail is too expensive for decoration. Hospitality only makes sense when it increases trust, frequency, margin, data, content, distribution, or acquisition efficiency.

This is where the investor conversation has changed, but still has not gone far enough.

Post-COVID, most investors learned the hard way that DTC online is not easy. The old story sounded beautiful: launch online, avoid retail, own the customer, scale with paid media, and build a higher-margin brand without the headaches of stores. Then CAC rose, iOS privacy changes made attribution worse, shipping became expensive, customer service ate into margins, and every category became crowded with well-packaged brands bidding for the same customer.

So investors are no longer naïve about pure DTC. They know the model can be fragile. But many still struggle with what comes next.

The answer is not simply to go back to old-school retail or to open restaurants for the sake of looking more “experiential.” The better answer is an omnichannel trust system: e-commerce for reach and repeat purchasing, retail for access and credibility, restaurants for trial and proof, content for demand creation, and data and supply chain for control.

That looks messy in a spreadsheet if each channel is valued in isolation. But for an operator, the channels are not isolated. They reinforce each other. A boutique may lower CAC, improve online conversion, support local delivery, create content, increase repeat purchasing, and make the brand more trusted. A restaurant may be a showroom, a sampling engine, a training ground, a product lab, and a credibility machine. If investors only underwrite it as a low-margin hospitality unit, they miss the strategic value.

The consumer journey is no longer clean. People discover on social, taste in restaurants, browse in stores, order online, reorder from email, and recommend in group chats. The brands that understand that journey may look less pure than the old DTC story, but they may also be more durable.

The internet is very good at creating awareness. It is less good at creating belief. Retail is very good at creating access. It is less good at explaining why a new brand deserves to replace an old habit. Restaurants, cafés, boutiques, and showrooms fill that gap because they give the customer a reason to care before asking them to convert.

The next generation of food brands will not be built only on shelves or screens. They will be built through systems of trust: digital for reach, retail for access, hospitality for experience, and e-commerce for repeatability.

The mistake of the DTC era was believing the internet could replace trust. The mistake now would be believing physical retail is just overhead.

For the right brands, the store is not the opposite of e-commerce. It is what makes e-commerce work.

Luis Mata

Flavors & Funders // CEO | Meat N’ Bone